|

|

|

The 2nd Powered and Next-Generation Cards Conference, organised by APSCA, was held on 17-18 July in Singapore. The first day focused on manufacturing next-generation cards. The second day was a Biometric Payment Card Seminar.

The 2nd Powered and Next-Generation Cards Conference, organised by APSCA, was held on 17-18 July in Singapore. The first day focused on manufacturing next-generation cards. The second day was a Biometric Payment Card Seminar.

Who was there

Who was there

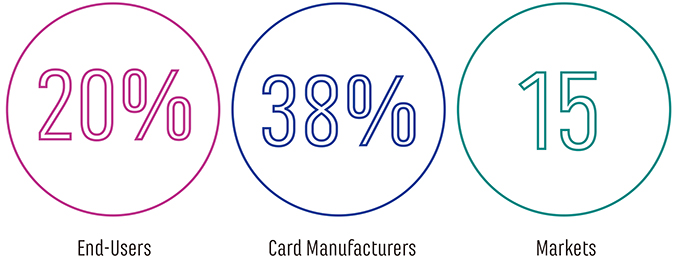

Participants from 15 markets in Asia, Europe and North America attended the conference. As well as leading card manufacturers, technology enablers and biometric sensor companies, the conference delegates came from payment card and transport card issuers, payment schemes and regulators learning about biometric payment cards.

Biometrics coming to cards

Industry development, standardisation work, certification progress and product evolution all point towards biometric cards becoming a new product category within 18 months. Consumer adoption of biometrics and the global transition to EMV contactless cards will drive biometric payment cards to become the first volume market for next-generation cards.

Pilots -> trials -> launches

Pilots -> trials -> launches

The complete status of global biometric card pilots, trials and launches was provided by: JCB, Mastercard and Visa; the leading biometric sensor developers; and by Antonio Albore in the Biometric Smart Cards 101 Tutorial. Commercial rollouts have so far focused on ID and access control. The first biometric payment card rollouts are expected in 2019.

More Conference Photos HERE

Key Conclusions from the Conference

-

The next-generation card business is maturing. Biometric smart cards now have real momentum and are expected to overtake the initial launches of DCVx card products and become the first mainstream next-generation card solution. The business case for biometric EMV contactless payment cards is particularly strong.

- New scheme requirements in many Asian markets mean that from October 2018 new acceptance terminals must be EMV contactless-enabled and new cards issued must support EMV contactless technology. The increased security and reduced friction offered by biometric EMV contactless payment cards supports this transition.

- Biometric EMV contactless payment cards prevent fraudsters from making payments on lost and stolen cards and remove the adverse media coverage and customer concerns raised by fraudsters on stolen card spending sprees. They also eliminate the possibility of so-called contactless skimming scams and related hacker claims.

- Biometric payment cards support the industry objective to phase out passwords. Replacing payment card and bank card PIN codes with on-card fingerprint biometrics eliminates PIN theft by fraudsters using shoulder surfing, miniature undetectable cameras near ATMs or payment terminals, or fake keyboards on ATMs.

- Biometric cards pave the way for high value contactless card payments. Today it is difficult or impossible for cardholders to make higher value EMV contactless card payments; PIN is not an intuitive fit with a contactless tap. Biometric on-card CVM supports EMV contactless card payments of any ticket size.

- In contrast to EMV migration and the introduction of contactless payments, biometric payment cards require no changes to existing POS infrastructure. Cardholders can immediately begin using their fingerprint instead of their PIN, as they have already learned to do with their smartphones, to verify their identity with every transaction.

- Customer biometric data is only stored on the card and never leaves the card, effectively addressing privacy concerns. Initial launches of biometric payment cards are enrolling customers at bank branches but home enrolment solutions using PC, tablet and smartphones are under development.

- Biometric payment cards now offer the same customer experience as legacy EMV cards with transaction times of less than 1 second, interoperability with existing EMV contact or contactless POS devices, and the same durability, lifetime and aesthetic appearance as the billions of EMV payment cards in use today.

- In contrast to PIN and signature-based cards, biometric cards identify the genuine cardholder. The False Acceptance Rate (FAR) of biometric smart cards is around 1 in 10,000, equivalent to a 4-digit PIN. A False Reject Rate (FRR) of less than 3% is considered acceptable with PIN as the fall-back CVM.

- Speakers from JCB, Mastercard and Visa explained that while mobile/digital payments are expected to increase, this still requires changing consumer behaviour. Consumers should be given the choice of a variety of payment solutions and cards will continue to be an important form factor.

- Feedback from the JCB biometric payment card pilot in Japan indicated that speed, security and convenience were highly rated. 87% of users found biometrics more convenient than PIN, 71% felt transaction times were the same as No CVM cards and 79% said that biometric CVM felt safer than PIN verification.

- The cost of biometric smart cards today is a factor, but not a barrier to their success. The critical success factor is the availability of technology. The answer to this is the industrialisation of the manufacturing process which will then lead to multiple manufacturers and in turn to volume manufacturing.

- The next critical success factor is an optimal consumer experience which will require: biometric EMV contactless cards without batteries (that do not require charging); sub-second transaction times with acceptable FRR; and effective, convenient and user-friendly remote enrolment solutions.

- Retail banking is the primary market for biometric smart cards, followed by financial inclusion and eID. Next-generation cards offer bank and payment card issuers an opportunity to acquire new clients, increase revenue, become top of wallet and position themselves as a payments innovator.

- Go-to-market strategies for biometric payment cards can focus on the benefits of improved customer experience, or greater convenience or stronger security. The increased security of a product that can only be used by the genuine cardholder is particularly relevant for ATM/debit cards.

- Most go-to-market strategies will benefit the issuer as well as the cardholder. Improving the customer experience of cross-border travellers through the ability to identify the genuine cardholder means there will be no need to reject valid transactions when your customers travel.

- ISO standards for biometric smart cards are well developed with standardisation activities beginning in 2002 and continuing in 2018. Application-level standardisation work on biometric EMV payment card products began more recently and is still being progressed by the international payment schemes.

- The first biometric EMV contact payment card products have been certified and launches are expected this year. The first certified biometric EMV contactless payment card products will be certified in early 2019 and biometric EMV contactless card products are expected to roll out in later next year.

|

Join the Next-Generation Cards Linkedin Group

Join the Next-Generation Cards Linkedin Group

The Next-Generation Cards Linkedin Group already has over 60 members! If you are with a payment card issuer or scheme, in a government ID agency, working for a transport authority or retailer, or with a fintech that wants to learn more about how cards fit with the digital future of payments and identity then join this group to meet domain experts from the world of next generation powered card solutions.

Click here to join the group!

|

|

|

|

|

|